Global Trade Policies Impacting US Automotive Imports by 6% in 2026

Advertisements

Global trade policies are projected to impact United States automotive imports by 6% in 2026, signaling a significant shift in market dynamics and strategic planning for manufacturers and consumers alike.

The automotive industry is a complex web of global supply chains, manufacturing hubs, and intricate trade agreements. Understanding how these elements interact is crucial, especially when facing significant shifts. This briefing delves into how Global Trade Policies Impacting United States Automotive Imports by 6% in 2026: A Market Briefing will reshape the American automotive landscape, affecting everything from vehicle availability to consumer prices. Prepare to navigate the nuanced world of international commerce and its direct implications for your next car purchase or business strategy.

Advertisements

Understanding the Current Landscape of US Automotive Imports

The United States has historically been one of the world’s largest importers of automobiles and automotive components. This extensive reliance on international markets has fostered a diverse selection of vehicles for consumers and supported a robust domestic auto industry through global supply chains. However, this interconnectedness also means that the US market is highly susceptible to shifts in global trade policies, which can ripple through the entire ecosystem from manufacturers to dealerships and, ultimately, to the end consumer.

The current landscape is characterized by a mix of long-standing trade agreements, recent adjustments, and ongoing negotiations. These policies dictate tariffs, quotas, and regulatory standards that directly influence the cost and availability of imported vehicles. Understanding these foundational elements is the first step in appreciating the projected 6% impact by 2026.

Key Trade Agreements Affecting Automotive Imports

Several pivotal trade agreements play a significant role in shaping US automotive imports. These agreements often aim to reduce trade barriers, but their terms can be complex and subject to change, leading to uncertainty in the market.

- USMCA (United States-Mexico-Canada Agreement): This agreement replaced NAFTA and introduced stricter rules of origin for automotive content, aiming to incentivize North American production.

- Bilateral Trade Deals: The US maintains various bilateral agreements with key automotive manufacturing nations, each with specific provisions for vehicle and parts imports.

- WTO Regulations: The World Trade Organization provides a framework for international trade, but disputes and differing interpretations can lead to tariffs and other trade barriers.

The interplay of these agreements creates a dynamic environment where policy adjustments can have widespread and immediate effects on import volumes and costs. The projected 6% impact for 2026 is a direct reflection of anticipated modifications and new policy implementations.

In conclusion, the foundation of US automotive imports is built upon a delicate balance of international trade policies. Any change, whether in tariffs, quotas, or rules of origin, inevitably sends tremors through this interconnected system, affecting the entire industry from manufacturing to sales.

The Mechanisms of Policy Impact: Tariffs, Quotas, and Regulations

Global trade policies exert their influence through a variety of mechanisms, primarily tariffs, quotas, and regulatory standards. Each of these tools can significantly alter the flow and cost of automotive imports into the United States, directly contributing to the projected 6% shift by 2026. Understanding how these mechanisms function is essential for grasping the real-world implications.

Tariffs, essentially taxes on imported goods, are perhaps the most direct and visible policy instrument. When tariffs on automobiles or auto parts increase, the cost for importers rises, which is often passed on to consumers. This can make imported vehicles less competitive compared to domestically produced alternatives, leading to a decrease in import volumes. Conversely, tariff reductions can stimulate imports by making them more affordable.

Quotas and Non-Tariff Barriers

Beyond tariffs, quotas impose quantitative restrictions on the volume of specific goods that can be imported over a certain period. If a country imposes a quota on a particular type of vehicle, once that limit is reached, no more of that vehicle can be imported until the next period. This directly curtails supply and can drive up prices for the available imported models.

- Import Quotas: These directly limit the number of vehicles or components allowed into the US, impacting availability and potentially increasing prices due to scarcity.

- Non-Tariff Barriers (NTBs): These include a wide range of regulations, such as stringent safety or environmental standards, complex customs procedures, or intellectual property protections. While not direct taxes, NTBs can significantly increase the cost and complexity of importing vehicles, acting as de facto trade barriers.

- Local Content Requirements: Some policies mandate that a certain percentage of a vehicle’s components must be sourced domestically or from specific trade bloc partners. This can force manufacturers to reconfigure supply chains, impacting import patterns.

Regulatory standards, while often implemented for consumer safety or environmental protection, can also act as trade barriers if they differ significantly from international norms. Manufacturers exporting to the US must ensure their vehicles meet American standards, which can require costly modifications or separate production lines for the US market. This adds to the cost of imports and can deter some foreign manufacturers from entering or expanding in the US market.

In summary, the combined effect of tariffs, quotas, and regulatory hurdles creates a complex matrix that shapes the economic viability and logistical feasibility of automotive imports. These policy tools are the primary drivers behind the anticipated changes in the US market.

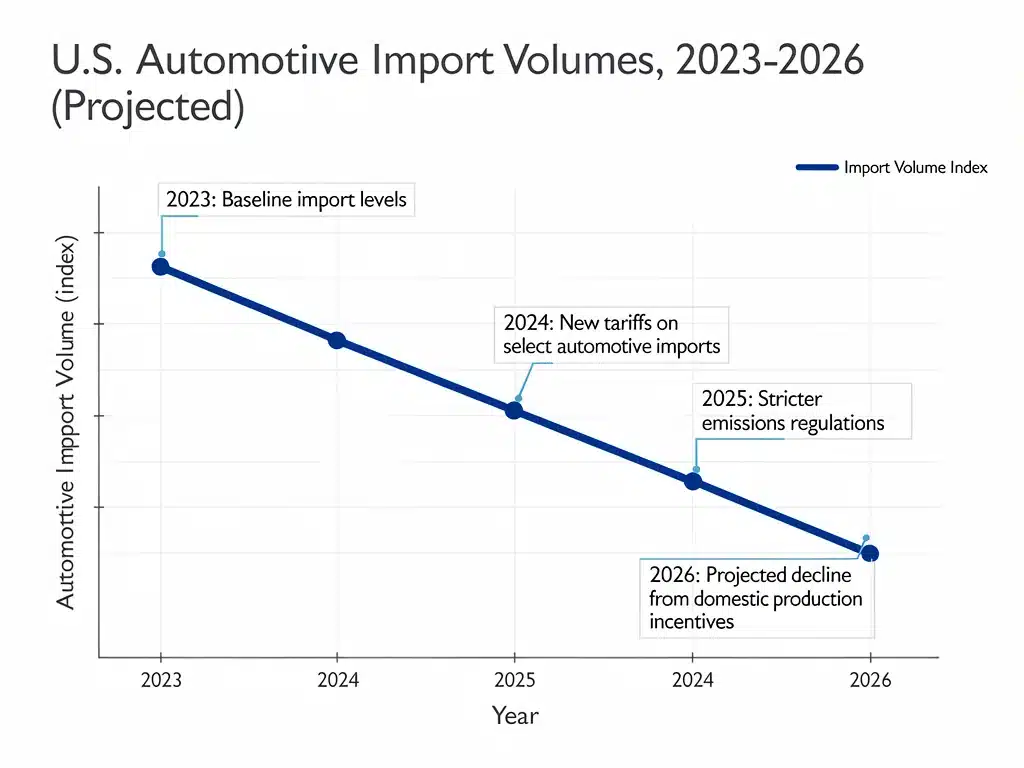

Projected Impact on Automotive Imports: The 6% Shift by 2026

The projection of a 6% impact on United States automotive imports by 2026 is not a static number but rather a dynamic forecast influenced by a confluence of evolving global trade policies. This anticipated shift represents a significant adjustment for the industry, potentially altering market shares, investment strategies, and consumer choices across the nation.

This 6% figure could manifest in various ways. It might represent a direct reduction in the total volume of imported vehicles, a shift in the origin countries of imports, or an increase in the average cost of imported automobiles due to higher tariffs or compliance expenses. The exact nature of the impact will depend on the specific policies enacted and how key trading partners respond.

Factors Driving the 2026 Projection

Several key factors are contributing to this projection. These include ongoing trade disputes, the renegotiation of existing agreements, and a global trend towards more localized or regionalized supply chains, often driven by national security or economic resilience concerns.

- Geopolitical Tensions: Escalating trade tensions between major economic blocs can lead to retaliatory tariffs and non-tariff barriers, directly affecting automotive trade flows.

- Domestic Production Incentives: Policies aimed at bolstering domestic manufacturing, such as tax credits for US-made electric vehicles, can indirectly reduce the demand for imports.

- Supply Chain Reshuffling: Lessons learned from recent global disruptions have prompted many companies to diversify or shorten their supply chains, potentially moving production closer to end markets like the US.

The 6% impact is a critical indicator for both policymakers and industry stakeholders. For policymakers, it highlights the tangible effects of their decisions on a major economic sector. For the automotive industry, it necessitates a re-evaluation of sourcing strategies, manufacturing locations, and market positioning. Companies that can adapt quickly to these policy-driven shifts will be better positioned to navigate the evolving market landscape.

Ultimately, the 2026 projection underscores the sensitivity of the US automotive market to global trade policy shifts. This anticipated change will demand strategic responses from all involved, from vehicle manufacturers to consumers.

Economic Repercussions for the US Automotive Market

The projected 6% impact on United States automotive imports by 2026 carries significant economic repercussions for the entire US automotive market. These effects will not be confined to a single segment but will ripple through various aspects, including consumer prices, domestic production, and the competitive landscape. Understanding these economic shifts is crucial for stakeholders to prepare and adapt effectively.

One of the most immediate and noticeable effects for consumers will likely be on vehicle pricing. If imports become more expensive due to tariffs or higher compliance costs, the price of both imported and, potentially, domestically produced vehicles could rise. This could reduce consumer purchasing power and shift demand towards more affordable options or used cars. The availability of certain models might also decrease, limiting consumer choice.

Impact on Domestic Production and Employment

While reduced imports might seem to benefit domestic production, the reality is more nuanced. Increased costs for imported parts, even for cars assembled in the US, can raise overall production expenses. However, if the policies genuinely incentivize domestic manufacturing and assembly, there could be an increase in jobs and investment within the US automotive sector.

- Increased Production Costs: Higher tariffs on components can increase the cost of manufacturing even domestically assembled vehicles, potentially impacting profitability.

- Shift in Investment: Foreign automakers might choose to invest more in US-based production facilities to circumvent import barriers, creating jobs and economic activity.

- Job Market Changes: While some manufacturing jobs might increase, jobs related to import logistics, sales of imported vehicles, or dealerships specializing in foreign brands could be affected.

The competitive landscape will also likely transform. Brands heavily reliant on imports might lose market share to those with stronger domestic production bases or more resilient supply chains. This could spur innovation in local manufacturing processes and supply chain management, as companies seek to mitigate policy risks. Furthermore, the used car market could experience increased demand and potentially higher prices if new car availability or affordability is constrained.

In essence, the economic repercussions are multifaceted, touching upon pricing, production, employment, and market competition. Navigating these changes will require careful strategic planning and adaptability from all participants in the US automotive market.

Strategic Responses from Automakers and Supply Chains

In anticipation of and response to the projected 6% impact on United States automotive imports by 2026, automakers and their intricate supply chains are already formulating and implementing strategic adjustments. These responses are critical for maintaining competitiveness, mitigating risks, and ensuring continued access to the lucrative US market. The strategies range from reconfiguring production networks to diversifying sourcing and investing in new technologies.

Many global automakers are re-evaluating their manufacturing footprints. This might involve shifting production of certain models or components closer to the US market to circumvent potential import tariffs or quotas. Such a move not only reduces trade policy exposure but can also shorten supply chains, making them more resilient to geopolitical disruptions and logistical challenges.

Diversification and Localization Efforts

Diversifying supply chains is another key strategy. Instead of relying heavily on a single country or region for critical components, automakers are working to establish multiple sourcing options. This reduces vulnerability to policy changes or disruptions in any one location.

- Regionalization of Production: Automakers are increasingly looking to establish or expand manufacturing facilities within North America to comply with rules of origin and reduce import exposure.

- Supplier Relationship Management: Strengthening relationships with domestic or regional suppliers is becoming a priority to ensure a stable and compliant supply of parts.

- Technological Investment: Investing in advanced manufacturing technologies, like automation and AI, can help optimize production efficiency and potentially offset higher labor costs associated with localized manufacturing.

Furthermore, some automakers are exploring new vehicle architectures that allow for greater flexibility in component sourcing. This could involve designing models that can easily integrate parts from various suppliers globally, or even developing platforms that are more suited for localized production. Research and development into alternative materials and production methods also plays a role in adapting to potential supply chain constraints.

In conclusion, the automotive industry’s strategic responses are multifaceted, focusing on resilience, compliance, and market proximity. These efforts are essential for navigating the evolving trade landscape and ensuring long-term viability in the US market.

Implications for Consumers and Future Vehicle Availability

The projected 6% impact on United States automotive imports by 2026 will undoubtedly have tangible implications for consumers, influencing everything from vehicle prices and available models to the overall car-buying experience. As global trade policies reshape the supply landscape, consumers will need to adapt to a potentially different market reality. Understanding these implications is key to making informed decisions in the coming years.

One of the most direct effects for consumers will be on vehicle pricing. Should tariffs increase or supply chains become more costly to navigate, the price of imported vehicles, and potentially even some domestically assembled cars that rely on imported parts, could rise. This might push certain models out of reach for some buyers or necessitate a re-evaluation of budgets. Conversely, increased domestic production spurred by policy could, in some scenarios, lead to more competitive pricing for US-made vehicles.

Changes in Model Availability and Options

Beyond price, the range and availability of vehicle models could also be affected. Automakers might prioritize importing certain models over others, or even cease importing less profitable models if trade barriers become too high. This could lead to a narrower selection of imported vehicles, potentially impacting niche markets or specific segments where foreign brands have historically dominated.

- Reduced Model Diversity: Consumers might find fewer imported models available, especially if specific brands or vehicle types become less economically viable to import.

- Longer Wait Times: Disruptions or reconfigurations in supply chains could lead to extended delivery times for both imported and some domestically produced vehicles.

- Increased Focus on Domestic Brands: A shift in market dynamics could encourage consumers to explore and favor US-made vehicles, potentially boosting sales for domestic manufacturers.

The overall car-buying experience might also change. Dealerships might face challenges in maintaining diverse inventories, leading to a greater emphasis on custom orders or a more localized selection. The long-term trend towards electric vehicles (EVs) could also be influenced, with policies potentially favoring domestically produced EVs through incentives, further steering consumer choices.

In summary, consumers should anticipate potential shifts in vehicle pricing, model availability, and the overall purchasing process. Staying informed about trade policy developments and their industry responses will be crucial for navigating the evolving automotive market.

Looking Beyond 2026: Long-Term Outlook and Adaptations

While the focus is currently on the projected 6% impact on United States automotive imports by 2026, it is imperative to look beyond this immediate horizon to understand the long-term outlook and the continuous adaptations required. Trade policies are rarely static, and the automotive industry’s response to these shifts will likely set new precedents for global manufacturing and supply chain resilience. The trends initiated by these policies will extend far into the future, shaping the industry for decades.

The period post-2026 is expected to see a continuation, and possibly an acceleration, of several key trends. One significant area will be the further regionalization of automotive supply chains. Companies will likely continue to invest in manufacturing capabilities closer to their primary markets, reducing dependence on distant and potentially volatile international routes. This doesn’t necessarily mean an end to global trade, but rather a more strategic and diversified approach to it.

Emerging Trends and Future Strategies

Technological advancements will also play an increasingly critical role. Automation, artificial intelligence, and advanced robotics in manufacturing can help offset higher labor costs associated with localized production, making regional hubs more competitive. Furthermore, the drive towards sustainability and electrification will likely intersect with trade policies, creating new incentives and challenges.

- Enhanced Supply Chain Resilience: The emphasis on robust, diversified, and regionalized supply chains will likely become a permanent fixture in automotive strategy.

- Technological Integration: Greater adoption of advanced manufacturing technologies will enable more flexible and efficient production closer to consumer markets.

- Policy Evolution: Future trade policies may increasingly incorporate environmental considerations, carbon border adjustments, and digital trade rules, adding new layers of complexity.

For the US market, this could mean a stronger domestic automotive industry, with increased investment in research, development, and manufacturing. However, it also means that consumers might need to adjust to different market offerings and pricing structures. The ability of both industry and government to anticipate and adapt to these evolving policy landscapes will determine the long-term health and competitiveness of the US automotive sector.

In conclusion, the long-term outlook suggests a continuous evolution driven by trade policies, technological innovation, and a global re-evaluation of supply chain strategies. Proactive adaptation will be key for all stakeholders in this dynamic environment.

| Key Impact Area | Brief Description |

|---|---|

| Import Volume Shift | Projected 6% impact on total US automotive import volumes by 2026. |

| Consumer Prices | Potential increase in vehicle costs due to tariffs and compliance expenses. |

| Supply Chain Adaptation | Automakers diversifying and regionalizing production to mitigate risks. |

| Domestic Production Boost | Incentives and policy shifts may drive increased US-based manufacturing. |

Frequently Asked Questions About US Automotive Imports and Trade Policies

Primary policies include tariffs, import quotas, and stringent regulatory standards such as safety and environmental requirements. Agreements like USMCA also play a crucial role by setting rules of origin and other trade conditions for vehicles and components.

A 6% impact could lead to increased vehicle prices due to higher import costs, tariffs, or reduced supply of specific models. Consumers might face fewer choices and potentially longer waiting periods for certain imported vehicles, influencing purchasing decisions.

The benefits are mixed. While some policies aim to boost domestic production and employment, increased costs for imported parts can also affect US-based assembly. The overall impact depends on specific policy details and each automaker’s supply chain strategy.

Automakers are diversifying supply chains, regionalizing production by investing in manufacturing closer to the US, and focusing on technological advancements like automation. These strategies aim to reduce reliance on single-source imports and mitigate tariff risks.

Trade policies could significantly influence EV availability, especially if incentives favor domestically produced EVs. This might lead to a greater focus on US-made electric models, potentially affecting the range of imported EV options and their pricing.

Conclusion

The projected 6% impact on United States automotive imports by 2026 underscores a critical juncture for the global automotive industry and the American market. This market briefing has highlighted how evolving global trade policies, manifested through tariffs, quotas, and regulatory standards, are poised to redefine the landscape of vehicle availability, pricing, and manufacturing strategies. Automakers are already implementing significant adjustments, from regionalizing production to diversifying supply chains, in a bid to navigate these complex changes. For consumers, this translates to potential shifts in vehicle affordability, model choices, and the overall car-buying experience. Looking beyond 2026, the long-term outlook suggests a continued emphasis on resilient, localized supply chains and technological integration, further shaping a more adaptive and potentially more domestically focused US automotive sector. The ability of all stakeholders to proactively respond to these dynamic forces will define success in this new era of global automotive trade.