Metal Prices Fluctuate: US Auto Costs Up 2% by 2026

Advertisements

The United States auto manufacturing sector is bracing for a projected 2% increase in costs by 2026, primarily driven by the ongoing volatility in metal prices, necessitating strategic adjustments across the supply chain.

Advertisements

The United States automotive industry is on the cusp of a significant financial shift. Projections indicate that metal prices auto manufacturing costs will rise by approximately 2% by 2026, a direct consequence of the unpredictable global metal markets. This impending increase demands a thorough understanding from manufacturers, suppliers, and consumers alike.

Understanding the Volatility in Metal Markets

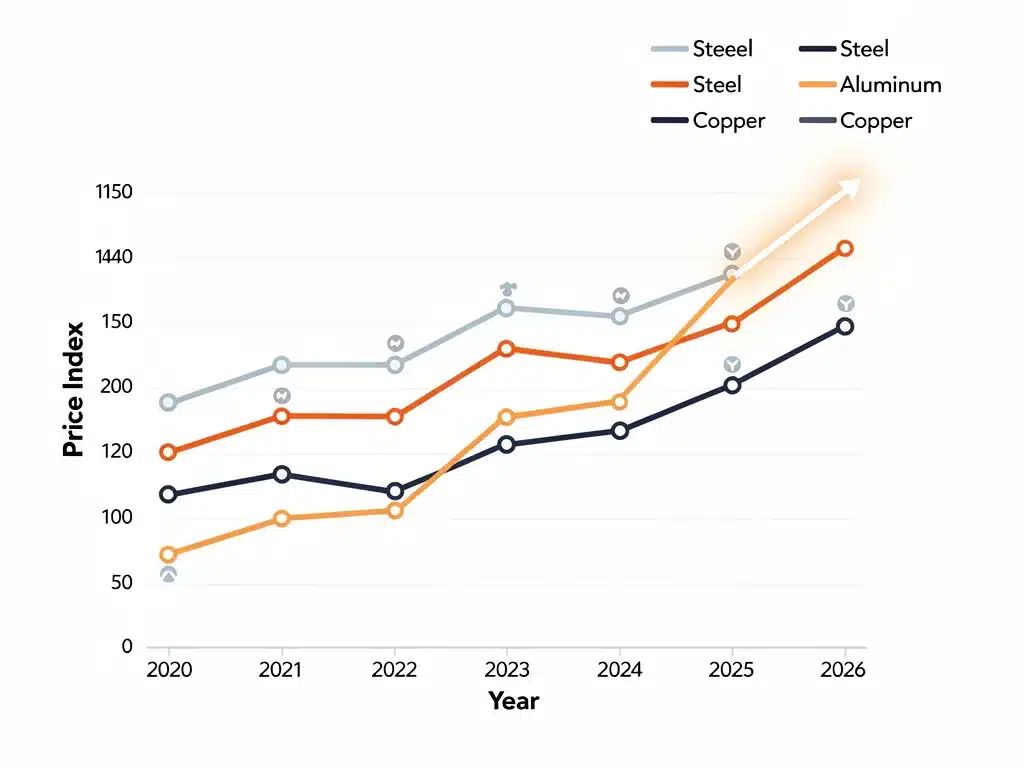

The global metal markets are intricate, influenced by a myriad of factors ranging from geopolitical tensions to shifts in demand and supply. For the automotive sector, which is heavily reliant on materials like steel, aluminum, copper, and specialty alloys, these fluctuations can have profound budgetary implications. Understanding the root causes of this volatility is the first step toward mitigating its impact.

Geopolitical Influences on Metal Supply

International relations and trade policies play a crucial role in the availability and pricing of raw materials. Tariffs, sanctions, and trade disputes can disrupt established supply chains, leading to scarcity and subsequent price hikes. Producers often pass these increased costs down the line, eventually affecting the end consumer.

- Trade tariffs and import duties directly inflate material costs.

- Political instability in key mining regions can halt production.

- International agreements and disagreements influence global market access.

Demand-Supply Dynamics and Economic Growth

The basic economic principles of supply and demand are always at play. Robust global economic growth often correlates with increased demand for industrial metals, pushing prices upwards. Conversely, economic slowdowns can lead to oversupply and price drops. However, the automotive industry’s consistent demand provides a baseline, making significant drops less likely in the long term.

Furthermore, the push towards electrification and sustainable technologies introduces new demand patterns. Electric vehicles (EVs) require different mixes of metals, such as increased copper for wiring and lithium/nickel for batteries, which adds another layer of complexity to price forecasting for traditional automotive metals.

Energy Costs and Environmental Regulations

Metal production is an energy-intensive process. Variations in global energy prices directly translate into higher or lower production costs for metals. Additionally, increasingly stringent environmental regulations around mining and smelting operations can add to operational expenses, which are then reflected in the final price of the metal. These regulations, while crucial for sustainability, present a cost challenge for the industry.

In conclusion, the volatility in metal markets is not a singular phenomenon but a complex interplay of geopolitical events, economic forces, and evolving industrial requirements. A holistic view of these factors is essential for any strategy aimed at managing the financial ramifications for the United States auto manufacturing sector.

Projected 2% Cost Increase: What It Means for US Auto Manufacturing

The forecast of a 2% increase in auto manufacturing costs by 2026, primarily due to metal price fluctuations, is a significant figure for an industry operating on tight margins. This seemingly small percentage can translate into billions of dollars across the entire sector, affecting everything from vehicle pricing to investment in innovation.

Direct Impact on Production Expenses

The most immediate effect of rising metal prices is on the direct cost of producing a vehicle. Steel, aluminum, and other metals constitute a substantial portion of a car’s material bill. A 2% increase on this fundamental input can quickly escalate overall production expenses, forcing manufacturers to make difficult decisions.

- Higher raw material costs directly impact bill of materials.

- Increased working capital needed to procure necessary metals.

- Potential for reduced profit margins if costs cannot be fully passed on.

Ripple Effect Across the Supply Chain

The impact isn’t confined to the major automakers. The entire supply chain, from tier-one suppliers producing complex components to smaller businesses manufacturing fasteners and specialized parts, will feel the squeeze. Each layer of the supply chain will likely face increased input costs, which then accumulate as they move up to the final assembly stage. This creates a cumulative effect that can be challenging to absorb.

Manufacturers will need to work closely with their suppliers to manage these rising costs, potentially renegotiating contracts or exploring new sourcing strategies. The interconnectedness of the automotive supply chain means that even minor price shifts can have widespread consequences throughout the industry, impacting numerous businesses and their employees.

Ultimately, a 2% cost increase represents a critical challenge for the United States auto manufacturing sector. It necessitates a proactive and adaptive approach to sourcing, production, and pricing strategies to maintain competitiveness and profitability in a dynamic global market. Understanding these implications is vital for strategic planning.

Strategic Responses from Automakers and Suppliers

Faced with the impending 2% cost increase, automakers and their suppliers are not standing idly by. They are actively exploring and implementing various strategic responses to mitigate the financial impact of volatile metal prices. These strategies often involve a combination of operational efficiencies, technological advancements, and innovative sourcing models.

Diversification of Sourcing and Supplier Relationships

One primary strategy is to diversify the sources of raw materials and components. Relying on a single or limited number of suppliers can expose manufacturers to significant risks during periods of price volatility or supply chain disruptions. By establishing relationships with multiple suppliers across different geographical regions, companies can build more resilient supply chains.

Furthermore, developing long-term partnerships with key suppliers can lead to more stable pricing agreements and collaborative efforts to optimize costs. These relationships often involve sharing market intelligence and jointly investing in research and development to find more cost-effective materials or production methods.

Technological Innovation and Material Substitution

Automakers are increasingly investing in research and development to find alternative materials or more efficient ways to use existing ones. This includes exploring lightweight composites, advanced plastics, and other non-metallic materials that can substitute for traditional metals in certain applications. Such innovations can reduce reliance on volatile metal markets while also potentially improving fuel efficiency and vehicle performance.

- Development of lighter, stronger alternative materials.

- Advanced manufacturing processes like additive manufacturing to reduce waste.

- Recycling initiatives to re-use existing metal resources more efficiently.

Hedging Strategies and Financial Instruments

To hedge against price fluctuations, some larger automotive companies utilize financial instruments such as futures contracts. These contracts allow them to lock in prices for future metal deliveries, providing a degree of predictability in their material costs. While hedging can be complex and carries its own risks, it can be an effective tool for managing exposure to market volatility.

In summary, the industry’s response to rising metal costs is multifaceted, combining a proactive approach to supply chain management, a commitment to technological innovation, and savvy financial planning. These strategies are crucial for navigating the challenges posed by unpredictable global commodity markets.

Impact on Vehicle Pricing and Consumer Choices

The projected 2% increase in auto manufacturing costs, largely driven by fluctuating metal prices, will inevitably have a cascading effect that reaches the end consumer. Automakers face the delicate balance of absorbing some costs to remain competitive and passing others along to maintain profitability, influencing vehicle pricing and, consequently, consumer choices.

Potential for Higher Vehicle Prices

When input costs rise significantly, manufacturers often have no choice but to adjust the sticker price of new vehicles. A 2% increase in manufacturing costs could translate into a noticeable rise in the retail price of cars, SUVs, and trucks. For consumers already grappling with inflation and economic uncertainties, this could make new vehicle purchases less accessible or attractive.

- Increased MSRP (Manufacturer’s Suggested Retail Price) for new vehicles.

- Higher financing costs due to larger principal amounts.

- Reduced affordability for certain vehicle segments, particularly entry-level models.

Shifts in Consumer Demand and Preferences

Higher vehicle prices can lead to shifts in consumer behavior. Buyers might opt for smaller, more fuel-efficient models that use fewer expensive materials, or they might delay new car purchases, extending the lifespan of their current vehicles. The used car market could also see increased demand as a more cost-effective alternative to new vehicles.

Moreover, the value proposition of electric vehicles (EVs) could be re-evaluated. While EVs often have higher upfront costs due to battery materials, their lower operating costs and potential for government incentives might become more appealing if conventional gasoline vehicles see significant price hikes. This could accelerate the transition to electric mobility for some segments of the population.

In conclusion, the impact of rising metal prices extends beyond the factory floor, directly influencing the showroom and consumer wallets. Automakers must carefully navigate pricing strategies to maintain market share while consumers will likely become more discerning, prioritizing value and long-term cost benefits in their vehicle purchasing decisions.

Government Policies and Industry Support

Recognizing the significant impact of fluctuating metal prices on a cornerstone industry like automotive manufacturing, governments and industry associations often step in to provide support and implement policies designed to stabilize markets or assist manufacturers. These interventions can range from trade policy adjustments to direct financial incentives and research funding.

Trade Policies and Tariffs Review

Governments can influence metal prices and availability through their trade policies. Reviewing and adjusting tariffs on imported raw materials or finished metal products can help alleviate cost pressures for domestic manufacturers. For instance, reducing import duties on steel or aluminum could lower the cost of these essential inputs for US automakers, making them more competitive globally.

However, such policies must be carefully balanced to protect domestic metal producers while supporting downstream industries. The goal is often to create a stable and predictable trade environment that benefits the entire supply chain without creating undue advantages or disadvantages for any single sector.

Subsidies, Grants, and Infrastructure Investment

Another form of government support comes through subsidies, grants, and investments in critical infrastructure. These can help manufacturers absorb some of the increased costs or invest in new technologies that reduce their reliance on expensive metals. For example, grants for research into alternative materials or more efficient manufacturing processes can indirectly mitigate the impact of rising metal prices.

Investment in domestic mining and refining capabilities can also reduce dependency on foreign sources, creating a more resilient and less volatile supply chain within the United States. This strategic investment benefits national security and economic stability.

Industry associations play a vital role in advocating for these policies and fostering collaboration among their members. They can provide platforms for sharing best practices, conducting joint research, and presenting a unified voice to policymakers regarding the challenges and needs of the automotive sector.

In summary, government policies and industry support are crucial elements in managing the economic fallout from volatile metal prices. Through strategic trade adjustments, financial aid, and collaborative initiatives, these entities can help ensure the long-term health and competitiveness of the United States auto manufacturing industry.

Long-Term Outlook and Adaptation Strategies

Looking beyond the immediate impact of the forecasted 2% cost increase, the United States auto manufacturing sector must develop robust long-term outlooks and adaptation strategies. The volatility in metal markets is unlikely to disappear entirely, making resilience and foresight paramount for sustained success and innovation in the coming years.

Focus on Circular Economy Principles

Embracing circular economy principles is a key long-term strategy. This involves designing vehicles for easier recycling, maximizing the use of recycled materials, and establishing efficient closed-loop systems for critical metals. By reducing reliance on newly mined raw materials, manufacturers can buffer themselves against price swings and contribute to environmental sustainability.

Investing in advanced recycling technologies and processes for automotive components, particularly for complex battery materials in EVs, will be crucial. This not only mitigates cost risks but also enhances resource security and reduces the industry’s environmental footprint, aligning with broader global sustainability goals.

Predictive Analytics and Market Intelligence

Advanced predictive analytics and sophisticated market intelligence systems will become indispensable tools for automakers. By leveraging data science, companies can better forecast metal price trends, anticipate supply chain disruptions, and make more informed purchasing decisions. This proactive approach allows for strategic inventory management and timely adjustments to production schedules.

- Utilizing AI and machine learning for price forecasting.

- Monitoring geopolitical and economic indicators for early warnings.

- Developing dynamic pricing models to adapt to input cost changes.

Collaborative Innovation Across the Ecosystem

The challenges posed by metal price volatility are too complex for any single entity to solve alone. Long-term adaptation requires collaborative innovation across the entire automotive ecosystem, including automakers, suppliers, research institutions, and even government bodies. Joint ventures, shared research initiatives, and open innovation platforms can accelerate the development of solutions.

This includes collaborating on new material science, optimizing manufacturing processes for greater efficiency, and developing common standards for material sourcing and recycling. A unified approach strengthens the industry’s collective ability to withstand future market shocks and drive sustainable growth.

In conclusion, the long-term outlook for United States auto manufacturing in the face of metal price fluctuations demands a strategic pivot towards circularity, data-driven decision-making, and unparalleled collaboration. These adaptation strategies will not only help manage costs but also position the industry for innovation and leadership in a rapidly evolving global landscape.

Navigating the Future: Resilience in Auto Manufacturing

The journey ahead for United States auto manufacturing is one that requires significant resilience and strategic agility. The projected 2% increase in costs due to fluctuating metal prices by 2026 is a clear signal that the industry must continuously evolve to maintain its competitive edge and ensure sustainable growth. This final section synthesizes the key takeaways and outlines a path forward for enduring success.

Embracing Agility in Supply Chain Management

The cornerstone of future resilience lies in building highly agile and robust supply chains. This means moving beyond traditional linear sourcing models to more dynamic, adaptable networks that can quickly respond to market shifts, geopolitical events, and unexpected disruptions. Diversification, both in terms of geographical sourcing and supplier relationships, will be paramount.

Furthermore, integrating advanced digital tools for real-time visibility into the supply chain will enable quicker decision-making and proactive risk mitigation. Manufacturers need to know where their materials are, understand potential bottlenecks, and have contingency plans ready to deploy at a moment’s notice. This level of transparency is essential for navigating unpredictable commodity markets.

Continuous Investment in R&D and Innovation

Innovation is not merely an option but a necessity. Continuous investment in research and development, particularly in material science and advanced manufacturing techniques, will be critical. Exploring and integrating new materials that offer cost stability, improved performance, or reduced environmental impact will provide a strategic advantage.

- Funding research into novel alloys and composite materials.

- Developing manufacturing processes that minimize waste and optimize material usage.

- Fostering partnerships with academic institutions and startups for groundbreaking solutions.

Policy Advocacy and Industry Collaboration

The automotive industry must continue to engage actively with policymakers to advocate for supportive trade policies, infrastructure investments, and regulatory frameworks that promote stability and growth. A unified industry voice can significantly influence governmental decisions that impact raw material access and cost structures. Collaboration among industry players, through associations and joint initiatives, will also foster collective strength.

Sharing best practices, pooling resources for common challenges, and working together on industry standards can elevate the entire sector. This collaborative spirit is vital for tackling complex issues like metal price volatility, ensuring that the United States remains a leader in global auto manufacturing.

In conclusion, the future success of United States auto manufacturing amidst fluctuating metal prices hinges on a combination of strategic adaptability, relentless innovation, and strong collaborative efforts. By embracing these principles, the industry can not only overcome the immediate challenges but also forge a path towards a more resilient, efficient, and sustainable future.

| Key Aspect | Brief Description |

|---|---|

| Cost Increase | US auto manufacturing costs projected to rise by 2% by 2026 due to metal price volatility. |

| Market Drivers | Geopolitical events, supply-demand, energy costs, and environmental regulations influence metal prices. |

| Industry Response | Diversified sourcing, material substitution, hedging, and R&D are key strategies. |

| Consumer Impact | Potential for higher vehicle prices and shifts in purchasing decisions. |

Frequently Asked Questions About Auto Manufacturing Costs

Steel, aluminum, and copper are primary metals highly susceptible to price fluctuations, directly impacting auto manufacturing costs. Specialty metals used in batteries for electric vehicles, such as lithium and nickel, also show significant volatility that affects the overall cost structure.

A 2% increase in manufacturing costs typically leads to higher MSRPs for new vehicles. While manufacturers may absorb some, a portion is usually passed to consumers, potentially increasing vehicle prices by hundreds to thousands of dollars depending on the model and its metal content.

Automakers are employing several strategies, including diversifying their metal sourcing, investing in material substitution and recycling technologies, and utilizing financial hedging instruments. They also focus on optimizing supply chain efficiencies and fostering stronger supplier relationships to stabilize costs.

Government policies, such as adjusting trade tariffs, offering subsidies for research and development, and investing in domestic mining, can play a role in stabilizing metal prices. These interventions aim to create a more predictable supply environment and reduce reliance on volatile international markets.

The cost increase could impact EV adoption, as EVs are heavily reliant on certain metals. While traditional vehicle prices may rise, the push for EV innovation might lead to new material discoveries or recycling efficiencies, potentially making EVs more competitive in the long run despite initial metal cost challenges.

Conclusion

The projected 2% increase in United States auto manufacturing costs by 2026, driven by fluctuating metal prices, represents a significant challenge for the industry. However, it also serves as a catalyst for innovation and strategic adaptation. Through diversified sourcing, technological advancements, smart financial planning, and collaborative efforts across the supply chain and with governmental bodies, the automotive sector can not only navigate these economic headwinds but also emerge stronger and more resilient, ensuring continued growth and competitiveness in the global market.