Semiconductor Shortage: 2026 US Vehicle Production Updates

Advertisements

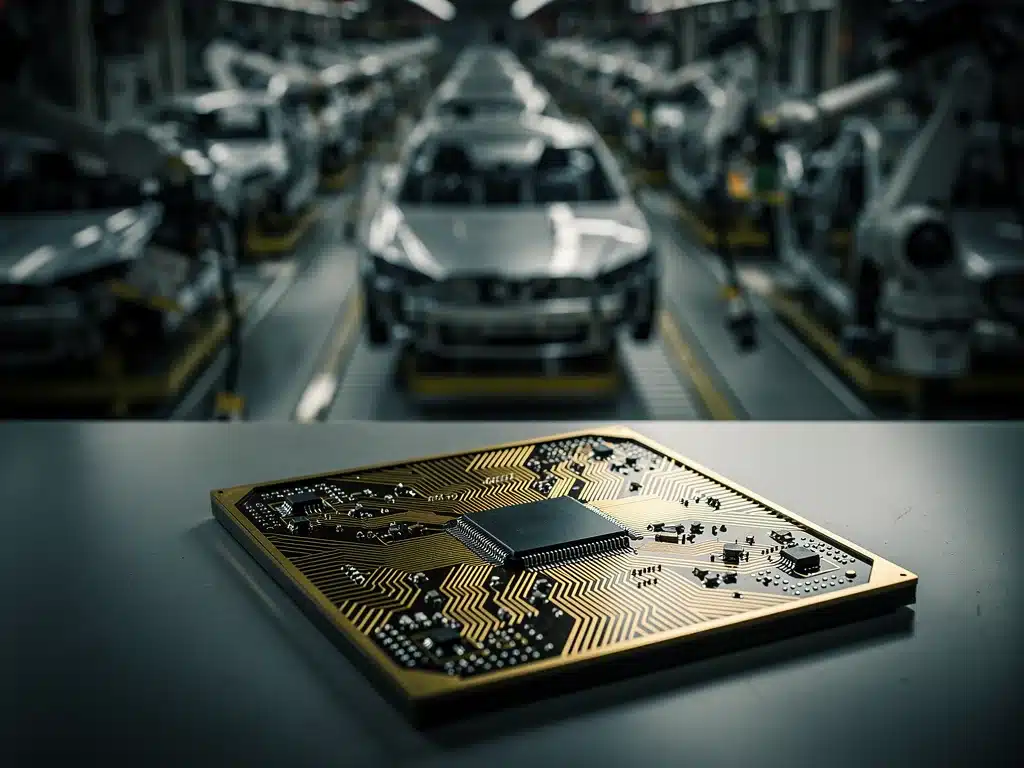

The ongoing semiconductor shortage continues to significantly disrupt 2026 vehicle production in the United States, forcing automakers to adapt strategies amidst persistent supply chain challenges and evolving consumer demand.

Advertisements

As we navigate the complexities of the global supply chain, the impact of the semiconductor shortage 2026 on vehicle production in the United States remains a critical concern. This persistent challenge is reshaping the automotive landscape, influencing everything from manufacturing schedules to consumer choices and driving innovation in unexpected ways. We’ll explore the latest market dynamics and what they mean for the industry and car buyers alike.

Understanding the Enduring Semiconductor Shortage

The semiconductor shortage, initially triggered by a confluence of factors including pandemic-induced factory shutdowns, surging demand for consumer electronics, and geopolitical tensions, has proven to be far more resilient than many industry experts initially predicted. What began as a temporary hiccup has evolved into a structural challenge, deeply embedded within the global manufacturing ecosystem. For the United States automotive sector, this means a continued struggle to secure essential electronic components, directly impacting vehicle output well into 2026.

Automakers rely heavily on semiconductors for a vast array of vehicle systems. From engine control units and infotainment systems to advanced driver-assistance systems (ADAS) and electric vehicle (EV) powertrains, these tiny chips are the brains behind modern automobiles. The complexity of these systems, coupled with the ‘just-in-time’ manufacturing philosophy prevalent in the auto industry, made it particularly vulnerable to any disruption in semiconductor supply. The ripple effect extends beyond mere production numbers, influencing vehicle features, pricing strategies, and even the types of vehicles prioritized for production.

Root Causes and Persistent Challenges

Several underlying factors contribute to the shortage’s longevity, creating a complex web of interconnected issues that are difficult to untangle. These aren’t simple problems with quick fixes, but rather systemic weaknesses exposed and exacerbated by recent global events.

- Legacy Chip Demand: Many automotive components utilize older, larger node semiconductors (28nm and above), which are less profitable for chip manufacturers to produce compared to cutting-edge chips for AI or smartphones.

- Geopolitical Tensions: Trade disputes and national security concerns have led to a push for localized production, but building new fabrication plants (fabs) takes years and billions of dollars.

- Capacity Constraints: The global semiconductor manufacturing capacity is finite, and expanding it requires significant capital investment and time, often several years from groundbreaking to full operation.

- Increased Electrification: The accelerating shift towards electric vehicles further intensifies demand for semiconductors, as EVs typically require more advanced and numerous chips than traditional internal combustion engine vehicles.

The persistence of the semiconductor shortage into 2026 underscores the deep-seated nature of these issues. Automakers are no longer simply waiting for the situation to resolve itself; they are actively seeking long-term solutions, from redesigning components to forging direct partnerships with chip manufacturers. This shift represents a fundamental change in how the automotive supply chain operates, moving away from past assumptions of readily available components.

Impact on 2026 US Vehicle Production Forecasts

The lingering semiconductor shortage continues to cast a significant shadow over 2026 vehicle production forecasts for the United States. Initial hopes for a full recovery by late 2024 or early 2025 have largely been tempered by the reality of ongoing supply chain volatility and escalating demand for chips across multiple industries. Analysts and automakers are adjusting their projections, indicating that production levels will likely remain below pre-pandemic highs, at least for the first half of 2026.

This sustained impact means that consumers can continue to expect higher prices, fewer available models, and potentially longer waiting times for new vehicles. Manufacturers are forced to make difficult decisions, often prioritizing higher-margin vehicles or those with strong demand, leading to an uneven distribution of inventory across dealerships. The ripple effect of reduced production extends throughout the automotive ecosystem, affecting not only assembly lines but also parts suppliers, logistics companies, and even car rental agencies.

Revised Production Estimates and Market Adjustments

Major automotive consulting firms and industry associations have released updated forecasts, painting a picture of cautious optimism mixed with persistent challenges. While some improvements in chip supply are anticipated, they are often offset by new demand spikes or unforeseen disruptions. This dynamic environment makes precise forecasting particularly difficult.

- Overall Production Volume: Estimates suggest 2026 US light vehicle production could still be 5-10% below ideal capacity, translating to millions of fewer vehicles compared to a fully optimized scenario.

- Segment Prioritization: Automakers are likely to continue prioritizing high-profit vehicles like full-size trucks and SUVs, as well as their expanding lineups of electric vehicles, which command higher prices.

- Inventory Levels: Dealership inventory is expected to remain lean, maintaining upward pressure on prices and reducing incentives for buyers.

- Regional Disparities: Production impacts may vary regionally within the US, depending on the specific models produced at different plants and their component requirements.

These revised forecasts highlight the need for continued adaptability within the industry. Automakers are exploring diverse strategies to mitigate the impact, from dual-sourcing chips to designing vehicles with more flexible electronic architectures. The goal is not just to survive the shortage but to emerge with a more resilient and agile manufacturing base, better prepared for future disruptions. The 2026 landscape will be defined by strategic resource allocation and a careful balancing act between meeting demand and managing limited supply.

Automaker Strategies to Mitigate the Shortage

In response to the prolonged semiconductor shortage, US automakers have implemented a range of innovative and pragmatic strategies designed to minimize production disruptions and maintain profitability. These approaches represent a significant departure from traditional supply chain management, emphasizing flexibility, direct engagement with suppliers, and even product redesign.

One of the most immediate tactics has been the strategic allocation of available chips. Manufacturers are prioritizing their most profitable models, such as large SUVs and pickup trucks, and increasingly, electric vehicles, which typically offer higher margins. This often means less popular models or lower trim levels might see longer delays or even temporary discontinuation. Furthermore, some automakers have opted to produce vehicles with missing non-critical components, intending to install them later once chips become available, though this adds logistical complexity and cost.

Innovative Supply Chain and Design Approaches

Beyond immediate allocation, automakers are investing in more fundamental changes to their operations and product development. This includes strengthening relationships with chip manufacturers and exploring long-term procurement agreements.

- Direct Supplier Engagements: Many automakers are bypassing traditional Tier 1 suppliers to establish direct contracts with semiconductor fabs, aiming to secure dedicated capacity.

- Component Redesign: Engineering teams are actively redesigning electronic control units (ECUs) to be compatible with a wider range of chips, including older generation or more readily available alternatives. This modularity reduces reliance on specific, hard-to-find components.

- Vertical Integration: Some larger automotive groups are considering or actively pursuing investments in semiconductor design or even manufacturing capabilities, aiming for greater control over their chip supply.

- Inventory Building: While ‘just-in-time’ was the mantra, many are now building strategic buffers of critical components, accepting the increased carrying costs as a necessary evil in a volatile market.

These strategies are not without their challenges, including significant capital outlays and the need for extensive collaboration across the supply chain. However, they are essential for navigating the current environment and building a more resilient automotive industry for the future. The focus has shifted from simply reacting to disruptions to proactively building systems that can withstand them, ensuring that the semiconductor shortage 2026 doesn’t derail long-term growth plans.

Technological Innovations and Future Resilience

The prolonged semiconductor shortage, while disruptive, has inadvertently spurred significant technological innovation within the automotive sector. Faced with limitations, engineers and designers are being pushed to create more efficient and adaptable vehicle architectures, laying the groundwork for greater resilience against future supply chain shocks. This period of constraint is accelerating the adoption of new technologies and methodologies that might have taken years to implement under normal circumstances.

One key area of focus is the development of more standardized and modular electronic platforms. By reducing the number of unique chip designs and increasing the interoperability of components, automakers aim to simplify their supply chains and gain greater flexibility. This could mean fewer distinct electronic control units (ECUs) performing multiple functions, or the ability to easily swap out one chip for a functionally equivalent alternative from a different manufacturer without extensive vehicle re-engineering.

Advanced Manufacturing and Design Principles

Beyond modularity, profound shifts are occurring in how vehicles are designed and how their components are sourced and manufactured. These changes are not just about coping with the current shortage but about building a fundamentally stronger and more agile industry.

- Software-Defined Vehicles: The trend towards software-defined vehicles (SDVs) allows for more functions to be controlled by software rather than dedicated hardware, potentially reducing the number and complexity of physical chips required. Updates and new features can be deployed over-the-air.

- New Materials and Packaging: Research into alternative materials for semiconductor packaging and interconnects could reduce reliance on scarce resources and improve manufacturing efficiency.

- AI-Driven Supply Chain Optimization: Artificial intelligence and machine learning are being deployed to predict demand fluctuations, identify potential bottlenecks, and optimize logistics, providing more foresight into supply chain vulnerabilities.

- Regional Manufacturing Hubs: The push for reshoring and friend-shoring semiconductor manufacturing is gaining traction, aiming to create more localized and secure supply chains, reducing dependence on single geographic regions.

These technological advancements are not merely reactive measures; they represent a proactive evolution of the automotive industry. The crisis has highlighted the need for robust, flexible, and technologically advanced solutions to ensure continuous production. By embracing these innovations, automakers hope to transform the challenge of the semiconductor shortage 2026 into an opportunity to build a more secure and innovative future for vehicle manufacturing.

Government and Industry Collaborative Efforts

Recognizing the critical national security and economic implications of the semiconductor shortage, both the US government and various industry consortia have intensified collaborative efforts. These initiatives aim to address the immediate supply crunch while simultaneously laying the groundwork for a more robust and resilient domestic semiconductor ecosystem. The understanding is that no single entity can solve this complex, global challenge alone, necessitating a coordinated, multi-faceted approach.

A cornerstone of the government’s strategy is the CHIPS and Science Act, enacted in 2022. This landmark legislation allocates significant funding to boost domestic semiconductor research, development, and manufacturing. The goal is to reduce reliance on foreign supply chains, particularly from East Asia, and to ensure a stable and secure supply of chips for critical industries, including automotive. This involves providing incentives for companies to build new fabrication plants and expand existing facilities within the United States.

Key Initiatives and Partnerships

Beyond legislative action, several partnerships and programs are underway, bringing together diverse stakeholders to tackle different facets of the shortage.

- Public-Private Partnerships: Government agencies are collaborating with leading chip manufacturers and automotive companies to identify critical needs and streamline regulatory processes for new fab construction.

- Workforce Development: Significant investments are being made in education and training programs to cultivate a skilled workforce capable of supporting advanced semiconductor manufacturing and research.

- International Cooperation: While prioritizing domestic production, the US is also engaging with allies to strengthen global supply chain transparency and resilience, recognizing the interconnected nature of the semiconductor industry.

- Research and Development Funding: Grants and incentives are being directed towards R&D for next-generation semiconductor technologies, aiming to keep the US at the forefront of innovation.

These collaborative efforts are crucial for navigating the challenges posed by the semiconductor shortage 2026. By fostering a supportive environment for domestic chip production and encouraging strategic partnerships, the aim is to create a more self-sufficient and secure supply chain. The success of these initiatives will be vital not only for the automotive industry but for the broader US economy and its technological leadership.

Consumer Impact and Market Adjustments in 2026

For the average American consumer, the enduring semiconductor shortage translates into a continued period of market adjustments in 2026. While the initial shockwaves of the shortage may have subsided, the long-term effects are now embedded in vehicle availability, pricing, and the overall purchasing experience. Consumers should anticipate a market that remains tilted in favor of sellers, characterized by sustained demand outstripping readily available supply.

New vehicle inventory levels are expected to remain tighter than historical averages, meaning fewer options on dealer lots and a reduced likelihood of finding significant discounts or incentives. This scarcity continues to drive up average transaction prices, making new cars more expensive. Furthermore, the used car market, which typically benefits from new car scarcity, is also likely to maintain inflated prices, as fewer new vehicles entering the market means less turnover of pre-owned models.

Buying Trends and Future Considerations

The shortage is not just affecting prices; it’s also influencing consumer behavior and purchasing decisions. Buyers are adapting to the new market realities, often with strategic shifts in their approach to vehicle acquisition.

- Longer Waiting Times: For popular models or custom orders, consumers may experience waiting periods extending several months, or even longer, depending on the specific vehicle and its component requirements.

- Reduced Customization: Automakers are simplifying options and trim levels to streamline production, meaning fewer choices for personalized vehicle configurations.

- Increased EV Adoption: Despite current EV production challenges, the long-term trend towards electrification continues, driven by fuel cost savings and environmental concerns, though availability can still be impacted by specific chip needs.

- Greater Focus on Maintenance: With new vehicles harder to come by, consumers are increasingly investing in extending the lifespan of their current vehicles through diligent maintenance and repairs.

Understanding these market dynamics is crucial for consumers planning a vehicle purchase in 2026. Flexibility in model choice, a willingness to consider pre-orders, and a realistic expectation regarding pricing will be key. The semiconductor shortage 2026 is compelling both buyers and sellers to adapt to a new normal, where patience and informed decision-making are more important than ever.

Long-Term Outlook and Industry Transformation

Looking beyond 2026, the semiconductor shortage is poised to fundamentally transform the automotive industry, fostering a new era of supply chain resilience, technological independence, and strategic partnerships. While the immediate challenges are significant, the long-term outlook suggests a stronger, more integrated, and perhaps more localized manufacturing base. This period of disruption is forcing a much-needed re-evaluation of established practices and accelerating trends that were already nascent before the crisis.

The ‘just-in-time’ inventory model, once a hallmark of efficiency, is being re-evaluated in favor of ‘just-in-case’ strategies, incorporating strategic stockpiles of critical components. This shift, while potentially increasing carrying costs, provides a crucial buffer against unforeseen disruptions. Furthermore, the drive towards greater transparency throughout the supply chain will become paramount, allowing automakers to identify and address vulnerabilities before they escalate into full-blown crises.

Building a Resilient Automotive Ecosystem

The lessons learned from the ongoing shortage are shaping a future automotive industry that is inherently more robust and adaptable. Several key transformations are expected to solidify in the coming years.

- Diversified Sourcing: Automakers will continue to diversify their chip suppliers, reducing reliance on single-source components and expanding their global procurement networks to mitigate regional risks.

- Strategic Investments: Expect sustained investment in domestic and allied-nation semiconductor manufacturing capabilities, driven by both government incentives and corporate strategic imperatives.

- Enhanced Collaboration: Deeper and more direct partnerships between automakers and semiconductor manufacturers will become the norm, fostering greater communication and shared risk.

- Flexible Vehicle Architectures: Future vehicle designs will prioritize modularity and software-defined functionalities, allowing for quicker adaptation to component availability and technological advancements.

The journey through the semiconductor shortage 2026 is not merely about overcoming a temporary hurdle; it’s about fundamentally reshaping the automotive industry for the decades to come. The industry is emerging from this period with a renewed focus on strategic autonomy, technological innovation, and a far more resilient supply chain, ensuring that future vehicle production can withstand a wider array of global challenges.

| Key Point | Brief Description |

|---|---|

| Persistent Shortage | Semiconductor supply issues continue to impact 2026 US vehicle production, defying earlier recovery predictions. |

| Automaker Adaptations | Manufacturers are prioritizing high-margin vehicles and redesigning components for chip flexibility. |

| Government Initiatives | The CHIPS Act and other programs aim to boost domestic semiconductor manufacturing and resilience. |

| Consumer Impact | Expect higher prices, limited inventory, and longer waiting times for new vehicles in 2026. |

Frequently Asked Questions About the 2026 Semiconductor Shortage

The shortage persists due to a combination of factors: demand for older chips used in cars, limited manufacturing capacity that takes years to expand, and increased chip requirements for electric vehicles and advanced features. These systemic issues are not quickly resolved.

Automakers are prioritizing production of high-margin vehicles, redesigning components to use more available chips, and forming direct partnerships with semiconductor manufacturers. They are also exploring modular vehicle architectures and building strategic component inventories.

Consumers should anticipate continued higher prices, limited new vehicle inventory, and potentially longer waiting times for specific models. Discounts and incentives are likely to remain scarce as demand continues to outpace supply in many segments.

Yes, the CHIPS and Science Act provides significant funding and incentives to boost domestic semiconductor research, development, and manufacturing. This aims to reduce reliance on foreign supply chains and secure a stable chip supply for critical industries, including automotive.

While some improvements are anticipated, a full resolution where supply consistently meets demand is not expected in 2026. Industry experts project a gradual easing, with significant improvements likely extending into late 2027 or even 2028 as new fabrication plants come online.

Conclusion

The persistence of the semiconductor shortage into 2026 continues to shape the United States automotive industry, presenting both significant challenges and compelling opportunities for transformation. While consumers face ongoing market adjustments in terms of availability and pricing, automakers are responding with innovative strategies, from redesigning vehicle architectures to forging closer relationships with chip manufacturers. Government initiatives, such as the CHIPS Act, underscore the national importance of addressing this issue, aiming to bolster domestic production and enhance supply chain resilience. Ultimately, the semiconductor shortage 2026 is not merely a temporary disruption but a catalyst for a more robust, technologically advanced, and strategically independent automotive ecosystem, poised for a more secure future.